What the 2025 Casino Boom Failed to Change: Player Behavior

Recommended casinos

A record number of new online casinos launched in 2025. Some targeted new markets. Others revived dormant licenses. Many vanished before year-end.

We tracked them. And we tracked how players responded.

Across regions, formats, and providers, one pattern held: player behavior didn't budge. More platforms entered the market, but engagement remained concentrated on the same titles, studios, and short-session play style that have shaped the industry since 2023.

This isn't about churn. It's about attention. And most new casinos didn't earn it.

Supply Scaled. Behavior Didn't.

The data is unambiguous.

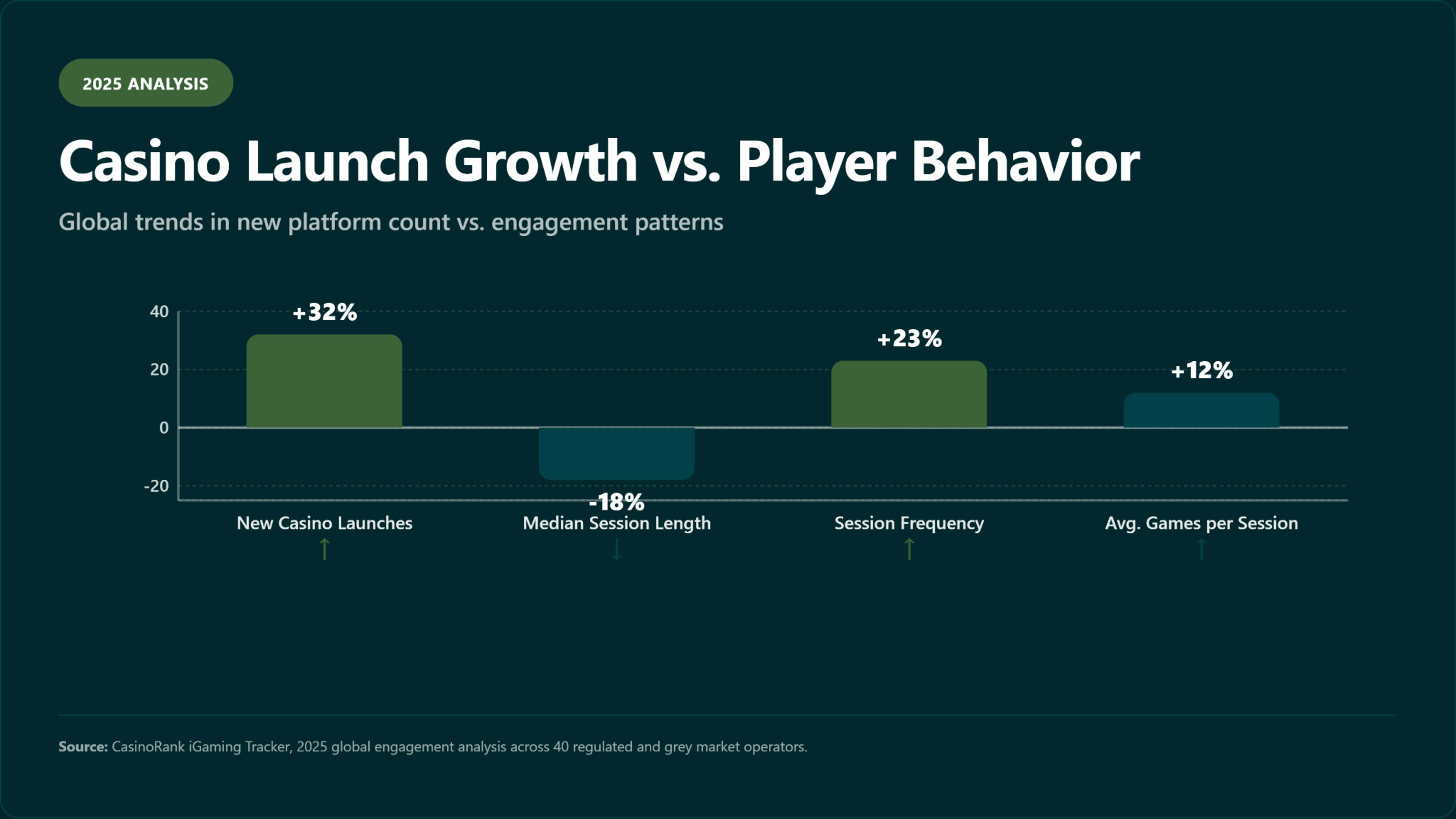

The number of new online casinos launched globally in 2025 increased by more than 30% compared with 2024. Europe and Latin America led in volume, while Asia and North America saw more controlled expansion.

Median session length dropped by 18%, while session frequency increased by 23%. Players logged in more often but stayed for shorter periods. The average number of games played per session remained flat at 3.2.

More than 80% of sessions involved only ten providers. Pragmatic Play alone accounted for 9 of the 10 most-played slots across all regions.

Most new casinos entered the market with the same content libraries, provider lineups, and UX structures. Player engagement followed familiar paths. The supply grew. The catalog widened. But behavior stayed focused.

This chart shows how the 32% surge in new online casino launches during 2025 had little impact on player behavior. While supply expanded, session length declined by 18%, frequency increased by 23%, and average games per session remained unchanged, indicating that player engagement remained concentrated.

Europe: More Brands, Same Habits

No region produced more new online casinos in 2025 than Europe. Across Malta, Sweden, Romania, and the Netherlands, we documented a steady stream of launches, many of which were white-label brands under recycled frameworks.

Malta remained the primary licensing hub. The Malta Gaming Authority processed applications throughout 2025, mostly for white-label operators. Sweden, despite tighter restrictions after 2024, continued to attract new entrants. Romania and the Netherlands drew operators seeking less saturated markets.

But player behavior didn't change:

- No new game cracked the top ten in regulated markets

- Pragmatic Play dominated with Gates of Olympus, Sweet Bonanza, and Big Bass Bonanza

- Gates of Olympus (launched in 2021) still generated the highest session volume

- Evolution's Lightning Roulette and Crazy Time controlled live dealer play

- Session composition: 3 games per visit, 60%+ repeat rate for the same titles

The few successful launches shared one trait: speed, load times under four seconds, familiar content front and center, zero friction. Technical performance mattered more than catalog size.

By Q3, consolidation was underway. Larger networks absorbed several white-label brands launched in early 2025. Customer acquisition costs and differentiation challenges made standalone operations unsustainable.

Latin America: Expansion Without Diversification

Latin America, especially Brazil, saw a regulatory inflection point in 2025. National legislation enabled the issuance of dozens of new licenses, and operators moved quickly.

Brazil's regulatory framework took effect in January 2025, establishing federal oversight by the Ministry of Finance. Brazil's PIX instant payment system has achieved near-universal adoption, making real-time deposits and withdrawals the norm. The conditions were right for expansion.

But user behavior looked familiar:

- 78% of tracked slot sessions in Brazil occurred on just five Pragmatic Play games

- Colombia and Argentina showed the same pattern with identical top titles

- 70%+ of casino play happened on mobile devices, sessions under six minutes

- Crash games stabilized at 8-12% of total volume, didn't displace traditional slots

- Bingo variants maintained engagement but didn't expand beyond existing bases

The issue wasn't access. It was differentiation. Most new casinos launched with identical libraries and no regional positioning. Players downloaded the apps, found the same games they were already playing elsewhere, and left.

Payment methods varied: PIX in Brazil, SPEI and OXXO in Mexico, and PSE in Colombia; however, payment diversity didn't translate into gameplay diversity.

Asia: Growth on Paper, Bottleneck in Practice

Asia's grey and regulated markets remain high-growth zones, especially Southeast Asia and India. In 2025, dozens of new platforms entered these regions, mobile-first, crypto-friendly, and focused on rapid onboarding.

The Philippines maintained its position as a licensing jurisdiction through PAGCOR. Curacao licenses remained common among grey-market operators. Cryptocurrency integration became standard, with platforms accepting Bitcoin, Ethereum, Tether, and regional stablecoins.

But user behavior followed the same pattern:

- Gates of Olympus, Starlight Princess, and Sweet Bonanza: 50%+ of all slot sessions

- Starlight Princess (2022 release) resonated in Southeast Asia with an anime-inspired aesthetic

- Providers without localized volatility, themes, and payment methods: under 10% re-engagement

- Platforms ignoring cultural UX norms (vertical screen, animated balances): day-one churn

- Western-themed slots with moderate volatility: failed to gain traction

Asia wasn't closed to new casinos. It was close to generic ones. Players wanted platforms that felt natively built for them, not translated versions of European designs.

The Indian market presented particular challenges. Regulatory ambiguity at the state level created a patchwork of legal frameworks. Operators navigated this by focusing on states with clearer regulations or positioning offerings as skill-based entertainment.

North America: Regulation Restrictions, Players Repeat

North America saw fewer new casino launches in 2025, largely due to regulatory constraints. West Virginia saw two additional operators launch. Connecticut added one new platform. Both markets remained smaller than those of mature jurisdictions such as New Jersey, Pennsylvania, and Michigan.

Engagement didn't shift:

- Evolution retained near-total control of live casino sessions in all licensed U.S. markets

- IGT, Light & Wonder, and Games Global topped session volume with proprietary slots

- New casinos showed identical catalogs and welcome flows

- Land-based brand recognition gave established operators advantages over pure online startups

Discovery wasn't just limited; it was pre-filtered. Without exclusive IP or unique onboarding mechanics, new platforms blended in. Players stuck with platforms they already trusted.

The tribal gaming market operated under different dynamics, leveraging existing customer relationships from land-based properties. The Canadian provinces Ontario, British Columbia, and Quebec followed similar patterns. Ontario's regulated market, which launched in 2022, matured in 2025 with slower growth as initial enthusiasm normalized.

This chart shows regional growth in new casino launches during 2025. Europe and Latin America led the expansion, while Asia and North America saw more limited activity.

Why Most New Casinos Didn't Move the Needle

The failure point wasn't the idea of the new. It was the execution.

This visual compares failed UX patterns with traits of high-performing casino launches in 2025. Speed, familiarity, and simplicity consistently outperformed large catalogs or complex flows.

What didn't work

- Long registration flows with multi-step verification before gameplay

- Cold lobbies without recognizable titles (obscure games didn't attract players)

- Slow load speeds (three-second delays meant abandonment)

- 2,000+ game catalogs with no filtering or intelligent organization

- Desktop UX patterns on mobile devices (didn't work in 70%+ mobile markets)

What worked

- Single-tap entry (biometric auth, saved credentials, social logins)

- Familiar games front and center (Gates of Olympus, Sweet Bonanza on home screen)

- Consistent game behavior across platforms (same loading, controls, timing)

- Mobile-first design (thumb-based interaction, portrait mode, optimized loading)

- Cultural alignment (high volatility for Asia, festive themes for Latin America)

Most new casinos didn't fail to attract users. They failed to retain them. Players came in, often more than once. However, without reinforcement, they reverted to what they already trusted.

2026 Outlook: Fewer Launches, Higher Expectations

Last year's surge proved unsustainable. We're now seeing the correction:

Volume Contraction

- Brands consolidating across all markets

- White-label networks shrinking client counts

- Customer acquisition costs are making standalone operations unsustainable

- Survivability matters more than time-to-market

Faster Failure Windows

- Most unsuccessful 2025 launches lost traction within five months

- New launches now show momentum indicators within 30 days

- Retention failures are obvious by day 60

- Operators are making go/no-go decisions faster

Higher Survival Thresholds

New platforms need:

- Load-to-first-play under 10 seconds

- Recognizable content immediately visible (Gates of Olympus, Sweet Bonanza front and center)

- Immediate personalization based on market data

- Loyalty programs reward frequency over duration

Differentiation Through Surfacing

Game count doesn't matter anymore. The battle is presentation, surfacing the right game at the right time to the right player. Successful platforms use session time, device type, play history, and patterns to predict optimal game presentation.

The Lessons from 2025

Last year showed what happens when a market scales without guiding user behavior. Hundreds of new casinos launched. Players didn't change.

That's not a failure. It's a constraint.

The constraint is attention. Players allocate their gambling attention to known quantities. They return to familiar games on familiar platforms. New casinos enter a market where attention is already distributed. Breaking into established attention patterns requires more than availability.

The future of new casino launches isn't bigger bonuses or longer catalogs. It's clarity. It's faster reward loops. It is the arrangement of content that captures attention. The platforms that survive won't just be new. They'll be necessary, for the player, not just the operator.

This timeline chart highlights how fast new casinos failed to retain users in 2025. Platforms now face a 60-day survival threshold, with viability judged by day 30.

If we want to build casinos that players actually choose, we need to stop designing for discovery and start designing for re-engagement.

2025 gave us scale. 2026 is forcing focus.

Sources:

Malta Gaming Authority – Annual report and licensing data (2025)

Ministério da Fazenda (Brazil) – National online gambling legislation framework (2025)

Statista – Global online casino session metrics (2024–2025)

PAGCOR (Philippines) – Licensing updates and regulatory environment

Ontario iGaming Market Report (iGO) – Year in review 2025

Curacao eGaming – Regulatory framework for 2025 licensees